Mortgages and Insurance

Outline what’s important to you.

We’ll help you get there.

Select one of the following products:

Where a great mortgage rate is just the beginning.

Financial, lifestyle and family goal driven solutions.

Our team is committed to your long-term financial success.

https://www.outline.ca/wp-content/uploads/2024/04/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-04-10 15:38:132024-04-10 15:45:20The Bank of Canada maintains policy rate

https://www.outline.ca/wp-content/uploads/2024/04/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-04-10 15:38:132024-04-10 15:45:20The Bank of Canada maintains policy rate https://www.outline.ca/wp-content/uploads/2024/04/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-04-03 20:57:172024-04-03 20:57:17Update on Ontario Budget 2024

https://www.outline.ca/wp-content/uploads/2024/04/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-04-03 20:57:172024-04-03 20:57:17Update on Ontario Budget 2024 https://www.outline.ca/wp-content/uploads/2024/02/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-02-01 21:00:052024-02-01 21:24:14January 2024: In the News

https://www.outline.ca/wp-content/uploads/2024/02/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-02-01 21:00:052024-02-01 21:24:14January 2024: In the News https://www.outline.ca/wp-content/uploads/2024/01/InTheNews-4.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

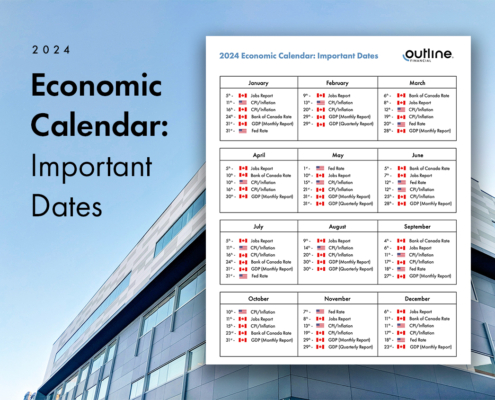

Jason Lang2024-01-25 20:17:252024-02-01 15:39:322024 Economic Calendar: Important Dates

https://www.outline.ca/wp-content/uploads/2024/01/InTheNews-4.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-01-25 20:17:252024-02-01 15:39:322024 Economic Calendar: Important Dates https://www.outline.ca/wp-content/uploads/2024/01/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-01-24 16:54:312024-01-25 20:24:38The Bank of Canada today held its target for the overnight rate at 5%

https://www.outline.ca/wp-content/uploads/2024/01/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2024-01-24 16:54:312024-01-25 20:24:38The Bank of Canada today held its target for the overnight rate at 5% https://www.outline.ca/wp-content/uploads/2023/12/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-13 12:02:232024-02-01 15:40:10OSFI maintains Minimum Qualifying Rate for uninsured mortgages

https://www.outline.ca/wp-content/uploads/2023/12/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-13 12:02:232024-02-01 15:40:10OSFI maintains Minimum Qualifying Rate for uninsured mortgages https://www.outline.ca/wp-content/uploads/2023/12/InTheNews-4.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-12 15:33:562024-02-09 00:28:48We are proud to announce that we have been named among the Best Mortgage Brokers by Canada Best!

https://www.outline.ca/wp-content/uploads/2023/12/InTheNews-4.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-12 15:33:562024-02-09 00:28:48We are proud to announce that we have been named among the Best Mortgage Brokers by Canada Best! https://www.outline.ca/wp-content/uploads/2023/12/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-07 15:09:092023-12-07 15:09:09Bank of Canada holds its policy interest rate steady, updates its outlook

https://www.outline.ca/wp-content/uploads/2023/12/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-12-07 15:09:092023-12-07 15:09:09Bank of Canada holds its policy interest rate steady, updates its outlook https://www.outline.ca/wp-content/uploads/2023/10/InTheNews-2.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-25 14:05:292023-10-26 13:47:58The Bank of Canada maintains policy rate

https://www.outline.ca/wp-content/uploads/2023/10/InTheNews-2.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-25 14:05:292023-10-26 13:47:58The Bank of Canada maintains policy rate https://www.outline.ca/wp-content/uploads/2023/10/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-17 19:39:282023-12-13 12:03:23‘Next move likely an interest-rate cut’ — What economists say about the latest inflation numbers

https://www.outline.ca/wp-content/uploads/2023/10/InTheNews-1.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-17 19:39:282023-12-13 12:03:23‘Next move likely an interest-rate cut’ — What economists say about the latest inflation numbers https://www.outline.ca/wp-content/uploads/2023/10/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-17 19:38:582023-10-24 19:39:09OSFI pulls back on some mortgage proposals, all in on others

https://www.outline.ca/wp-content/uploads/2023/10/InTheNews.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-10-17 19:38:582023-10-24 19:39:09OSFI pulls back on some mortgage proposals, all in on others https://www.outline.ca/wp-content/uploads/2023/09/InTheNews-2.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-09-25 16:04:442023-09-25 16:04:45No rate hike? No time like the present then to regroup and reset

https://www.outline.ca/wp-content/uploads/2023/09/InTheNews-2.jpg

845

1080

Jason Lang

https://www.outline.ca/wp-content/uploads/2019/08/websitelogo.png

Jason Lang2023-09-25 16:04:442023-09-25 16:04:45No rate hike? No time like the present then to regroup and resetOutline Financial is one of Canada’s top-rated mortgage and insurance companies offering direct access to rate and product options from over 30 banks, credit unions, mono-line lenders and insurers all in one convenient service. The Outline team was formed by senior level bankers and financial planners that wanted to offer clients choice with an exceptional service experience.